BotR — Automated ES Futures Strategy

Adaptive rule-based strategy for ES and MES futures. 60-minute timeframe, 8 AM–5 PM ET session, 2–4 trades per week. Self-optimizing exits and multi-layer risk controls.

30-Day Money-Back Guarantee (monthly plans) · Cancel anytime.

Methodology

BotR is a rule-based system — every decision is governed by defined logic. No discretion, no manual overrides.

Targets breakout and range-expansion conditions on the 60-minute ES/MES chart. Market classification (breakout, trap, range) determines whether a signal qualifies for entry. Score-based filtering eliminates low-probability setups.

Self-optimizing exits adapt to live momentum. If momentum fades mid-trade, exits tighten automatically. All positions close at session end (5:00 PM ET) — no overnight exposure under any circumstance.

Daily loss caps, maximum consecutive loss limits, and contract size controls are all hard-coded. The strategy enforces these at the engine level — they cannot be overridden by market conditions.

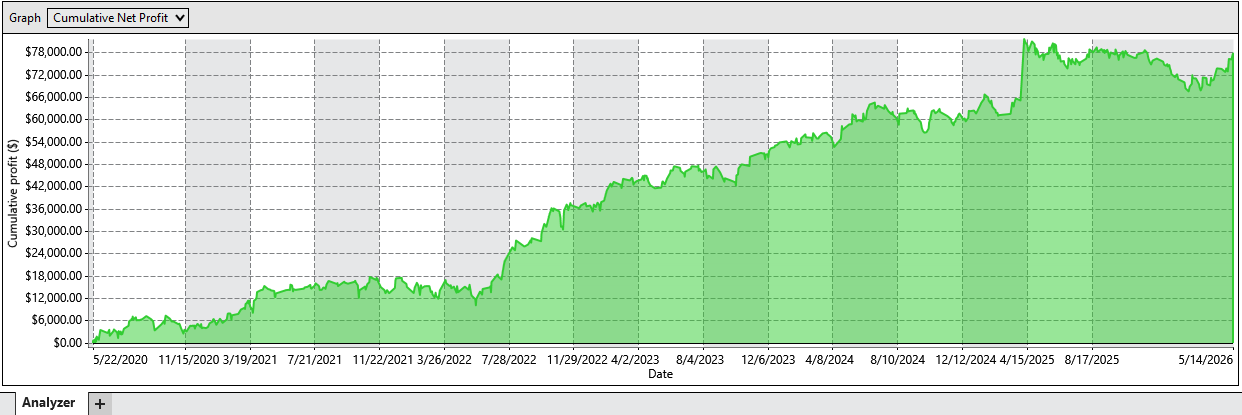

Performance History

6-year backtest on ES futures (60-minute timeframe), May 2020 – May 2026. Commission and slippage included.

May 2020 – May 2026 — 6-year backtest, 1 ES contract, 60-minute timeframe · commission + slippage included

See every backtested trade →How BotR Works

Built for volatility — targets breakouts during sessions with expanding range

BotR is an adaptive, rule-based trading system engineered for the E-mini S&P 500 (ES) and Micro E-mini S&P 500 (MES) futures markets. Operating on the 60-minute timeframe during the 8:00 AM – 5:00 PM ET session, it executes 2–4 trades per week — selective by design, targeting only the highest-probability setups.

The strategy uses real-time market classification — identifying breakout, trap, and range conditions — and adapts stops, targets, and sizing based on live conditions and historical performance. Score-based exit logic lets BotR self-correct mid-trade when momentum fades, while daily loss caps, max consecutive loss limits, and contract size controls keep risk in check.

BotR is built for volatility. It is engineered to capture large range-expansion moves rather than to win on every trade — selectivity and asymmetric exits are the core of its edge. The 6-year backtest window (May 2020 – May 2026) deliberately spans the 2020 volatility shock, the 2022 bear market, and the 2025 volatility regime — the conditions the strategy is designed to trade. Backtested results are hypothetical and include commissions and slippage; past performance does not guarantee future results.

All positions are closed at session end — no overnight risk. Once installed in NinjaTrader 8, BotR runs fully autonomously. Connect it to your broker, set your contract size (ES or MES), and it handles entries, exits, and risk management without any manual intervention.

What You Need to Run BotR

Make sure your setup meets these requirements before subscribing. If you have questions, check the FAQ or contact support.

Start Trading BotR

No contracts. Cancel anytime.

$99/mo · Billed $891/year · 3 months free

30-Day Money-Back Guarantee

- BotR NinjaScript algorithm file

- Step-by-step PDF setup guide

- Full backtest data and performance reports

- All built-in risk management controls

- All future updates to BotR

- Discord community access + support

BotR — Frequently Asked Questions

BotR trades ES (E-mini S&P 500) and MES (Micro E-mini S&P 500) futures on NinjaTrader 8, on the 60-minute timeframe during the 8:00 AM – 5:00 PM ET session.

BotR averages 2–4 trades per week (approximately 0.5 trades per day). It is selective by design — quality over quantity is a core principle of the strategy's edge.

No. BotR closes all positions at session close (5:00 PM ET) every day. There is zero overnight risk.

Most traders have BotR running in under 10 minutes. After subscribing, you receive the NinjaScript file and a step-by-step setup guide. The setup involves importing the strategy file into NinjaTrader and configuring your contract size (ES or MES) and broker connection.

BotR was backtested on the 60-minute ES futures chart from May 2020 to May 2026 (a 6-year period), trading 1 ES contract at a time, run in NinjaTrader's Strategy Analyzer. The backtest includes all commissions and slippage — these are realistic figures, not idealized. Results are scalable — MES traders can run the same logic at 1/10th the position size. The test recorded 796 total trades across the full 6-year period.

HYPOTHETICAL PERFORMANCE RESULTS HAVE MANY INHERENT LIMITATIONS, SOME OF WHICH ARE DESCRIBED BELOW. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFITS OR LOSSES SIMILAR TO THOSE SHOWN. IN FACT, THERE ARE FREQUENTLY SHARP DIFFERENCES BETWEEN HYPOTHETICAL PERFORMANCE RESULTS AND THE ACTUAL RESULTS SUBSEQUENTLY ACHIEVED BY ANY PARTICULAR TRADING PROGRAM. ONE OF THE LIMITATIONS OF HYPOTHETICAL PERFORMANCE RESULTS IS THAT THEY ARE GENERALLY PREPARED WITH THE BENEFIT OF HINDSIGHT. IN ADDITION, HYPOTHETICAL TRADING DOES NOT INVOLVE FINANCIAL RISK, AND NO HYPOTHETICAL TRADING RECORD CAN COMPLETELY ACCOUNT FOR THE IMPACT OF FINANCIAL RISK IN ACTUAL TRADING. FOR EXAMPLE, THE ABILITY TO WITHSTAND LOSSES OR TO ADHERE TO A PARTICULAR TRADING PROGRAM IN SPITE OF TRADING LOSSES ARE MATERIAL POINTS WHICH CAN ALSO ADVERSELY AFFECT ACTUAL TRADING RESULTS. THERE ARE NUMEROUS OTHER FACTORS RELATED TO THE MARKETS IN GENERAL OR TO THE IMPLEMENTATION OF ANY SPECIFIC TRADING PROGRAM WHICH CANNOT BE FULLY ACCOUNTED FOR IN THE PREPARATION OF HYPOTHETICAL PERFORMANCE RESULTS AND ALL OF WHICH CAN ADVERSELY AFFECT ACTUAL TRADING RESULTS.

For full risk disclosure, see our Risk Disclosure page.